49 Wealth

Fix

There’s a straight line between wealth concentration, corporate consolidation, and the strategy of ‘buying, not building’. In short, Peter Thiel is correct when he says that ‘competition is for losers’.

Speaking of competition and losers, Ronald Reagan set the tone of the neoliberal era when, in 1981, he fired 11,000 striking air-traffic controllers. The message? Workers were losers who would be subjected to the discipline of competition. Reagan called it ‘morning in America’. But really, it was ‘morning for American big business’.

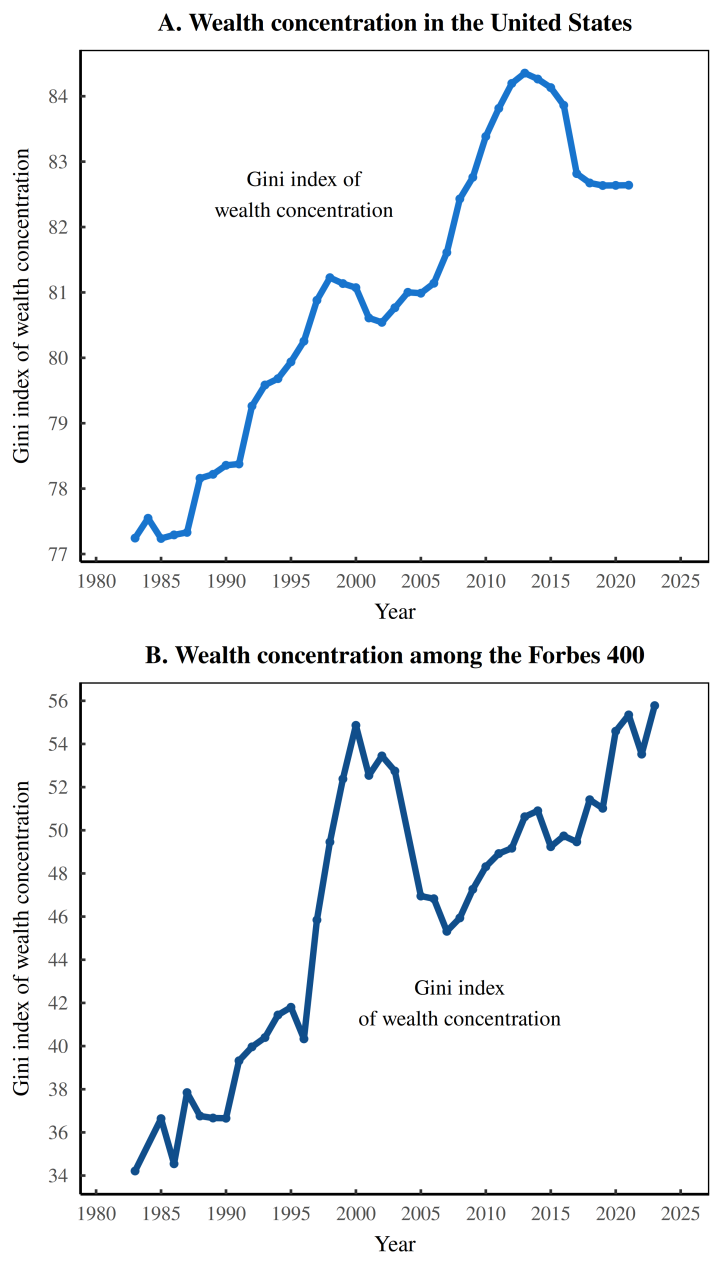

Today, we are well into the next-day’s hangover, and we know how the party played out. For workers, it was a disaster. But for the rich, it was an incredible boon. Wealth didn’t trickle down so much as it got catapulted up. The result, as Figure 1A shows, was a relentless rise in the concentration of American wealth.

As wealth got catapulted from the poor to the rich, it also got transported from the mega rich to the supremely rich. Even among the upper crust of elites wealth has grown more concentrated. The culprit seems to be the stock market.

The world’s billionaires have a median wealth of about $2.4 billion. Compared to the $240B wealth of the world’s richest man, Elon Musk, $2.4B is chump change.

The fit between the S&P 500 and billionaire wealth concentration is so tight. S&P 500 tracks the total market capitalization of the 500 largest US firms. S&P 500 sums the market capitalization of the 500 largest US firms.

To unwrap our stock-market puzzle, we need to review some math. In general, measures of spread are unrelated to measures of central tendency. There is, however, an exception. It happens when growth is driven by inequality. ‘Growth through inequality’ — explains our stock-market results. The S&P 500 index (an average) is connected to levels of elite wealth concentration (a form of spread). But this connection only makes sense if the S&P 500 is an (unwitting) indicator of stock-market inequality.

What appears as stock-market ‘growth’ is in part, an artifact of rising stock-market concentration. As their stock rises, the richest firms will buoy the whole S&P 500 index. But this buoyancy isn’t really ‘growth’; it’s an artifact of corporate concentration — rich firms getting richer.

The ‘crime’ of elite wealth concentration seems to be tied directly to corporate oligarchy.

Savvy corporations are always looking for a better route to power. And that better route is to buy instead of build.

Google’s success stories (its ad-tech stack, its mobile platform, its collaborative office suite, its server-management tech, its video platform …) are all acquisitions.

Billionaires like Peter Thiel are so hubristic that they speak brazenly about their pursuit of power, laying bare their inner robber baron. The upshot to this plute bravado is that few people will be surprised by the straight line that connects corporate oligarchy with the concentration of elite wealth.