46 Saudi Arabia

Tverberg

Saudi Arabia does not seem to be using recent record profits to quickly raise reinvestment to the level that seemed to be required a few years ago. This suggests that Saudi Arabia needs prices that are quite a bit higher than $100 per barrel in order to take significant steps toward extracting the country’s remaining resources.

Tverberg (2022) Why No Politician Is Willing to Tell Us the Real Energy Story

Messler (2022) Saudi Aramco Is Taking A Page Out Of The U.S. Shale Playbook

Smith

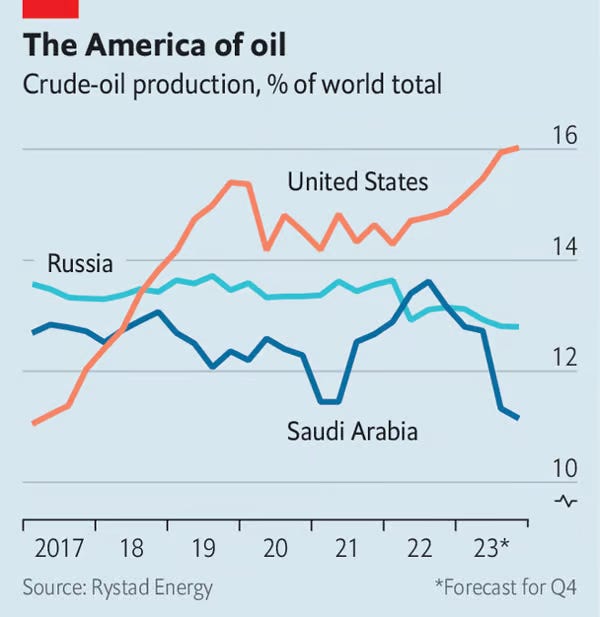

Traditionally, people thought that Saudi Arabia was the world’s crucial “swing producer” of oil. The basic idea was that even though Saudi was far from a monopolist in the global oil market, they were the only producer who could increase or decrease production by huge amounts in a very short time frame. And so it was thought that the Saudis could basically control global oil prices, both because global demand is inelastic (meaning that modest swings in production can change prices a lot) and because the other OPEC countries would follow the Saudis’ lead.

But in recent years, another key swing producer has emerged: the United States. Since around 2010, the biggest swing by far has been the rise of U.S. shale oil production. And even as the Saudis have slashed production in 2023, the U.S. has raised its own oil output by almost as much.

The U.S. is winning the tug-of-war. Saudi has cut production, but prices have gone down anyway. The combination of fewer barrels sold and fewer dollars per barrel is dealing a crushing blow to the Saudi economy. The country is now in a recession, with GDP shrinking at a stupendous 4.5% annualized rate in the third quarter.

The Saudis are in big trouble. Their ability to push oil prices around like a monopolist is gone, so cutting production simply impoverishes them. That’s bad news for a country that has seen zero GDP growth in 30 years.